Foreclosures are rising across the United States, and for many families, this is already a reality. In this video, we take a closer, more human look at what’s really happening behind the numbers. From rising mortgage payments and job loss to increasing living costs, more people are finding themselves in situations they never expected to face. As we react to a series of TikTok clips, the focus isn’t just on statistics, but on the emotional weight of what people are going through. You’ll hear stories of individuals on the brink of losing their homes, families asking for help, and homeowners sharing how quickly things can spiral when life becomes more expensive.

These moments highlight how fragile financial stability can feel in today’s economy. We also explore the growing conversation around veteran foreclosures, where those who once served their country are now struggling to keep a roof over their heads. Whether it’s policy changes, financial hardship, or broken expectations, these stories raise deeper questions about trust, stability, and support systems in uncertain times. Another key theme in this video is the idea that this housing crisis feels different from past ones. Many homeowners aren’t losing their properties due to reckless decisions, but because costs like insurance, taxes, and basic living expenses have increased faster than income.

It’s a quieter kind of pressure, but one that’s affecting millions of people. Throughout the video, we reflect on what these stories reveal about modern life — the shrinking margin for error, the stress of staying afloat, and the importance of being prepared for the unexpected. This is about understanding the reality many people are facing and recognizing that you’re not alone if you’ve been feeling the pressure too. If you’ve noticed changes in your own financial situation, or if these stories resonate with you in any way, feel free to share your thoughts in the comments. Your perspective matters, and these conversations can help others feel less alone during difficult times.

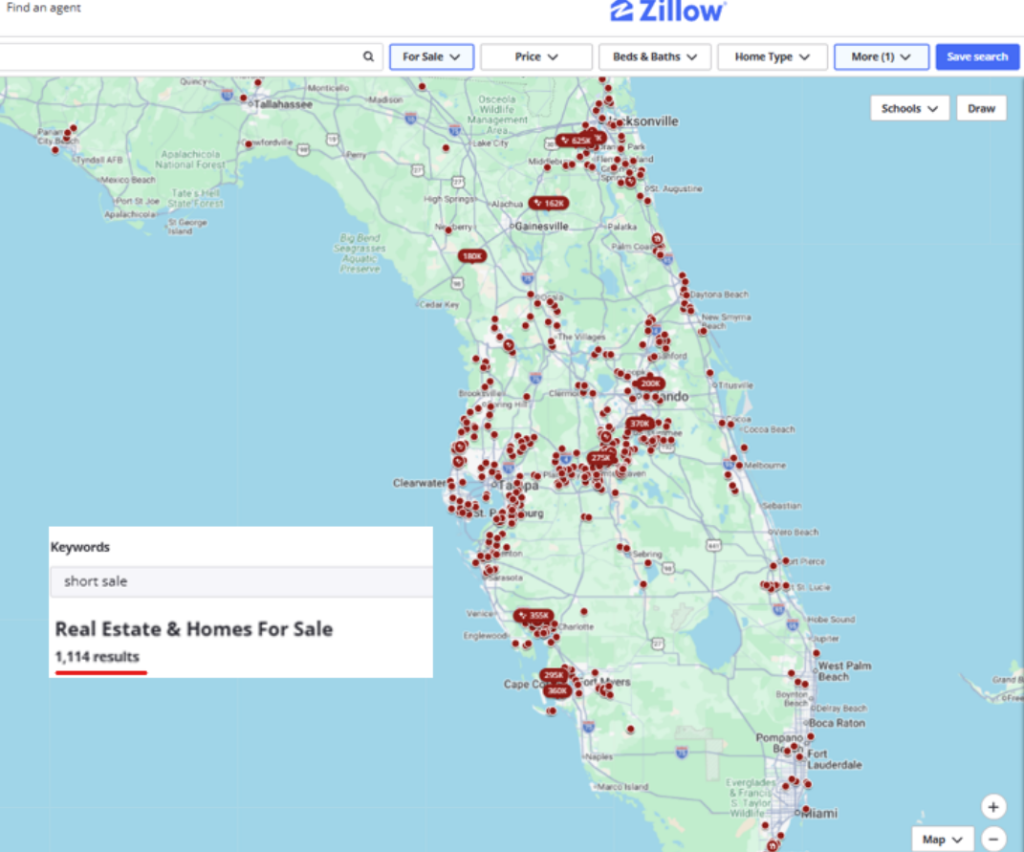

- Over 1,000 Florida homes now have “short sale” in their listing descriptions. Many at $100,000+ discounts from their previous sale price. Florida foreclosures up 43% YoY in Q1 2026. ATTOM data shows REOs (bank-owned properties) doubled from 487 to 1,014 in 12 months. Florida now has the nation’s highest foreclosure rate — one filing for every 230 housing units in 2025. This isn’t 2008. It’s something else. Worth understanding what. Here’s what’s actually happening in Florida housing. The statewide FHFA House Price Index fell 2.3% YoY through Q3 2025, while the national index rose 2.2%. That’s a 4.5-point gap. Tampa Case-Shiller is down 3.9% YoY with 13 consecutive months of annual declines — the steepest of any city in the 20-metro composite. Condo markets are in outright distress. Statewide supply: 13.2 months (a balanced market is 5-6 months). Prices down 6.1% YoY. 92% of major condo markets declining. Some Miami-area condos are selling for 30-40% below 2022 peaks. Single-family inland markets are holding up better. Jacksonville is roughly flat. The Orlando area is fine. Palm Beach County single-family medians hit new highs (+7.7%). This isn’t a statewide crash. It’s geographically and structurally specific. Three forces driving the distress. First: insurance costs. Florida homeowners pay 181% above the national average for property insurance. Cape Coral has the third-highest premium-to-market ratio in the nation at 2.2% — meaning a $350,000 home costs $7,700 annually in insurance alone. For owners in hurricane-exposed markets, insurance has become a larger monthly expense than the mortgage principal on newer homes.

- When insurance spikes 20-30% in a single year (which has happened repeatedly since 2022), marginal homeowners can’t absorb it. Second: post-Surfside condo reserve mandates. After the 2021 Surfside collapse, Florida law now requires older condos to conduct structural inspections and maintain adequate reserves. Thousands of condo associations are issuing six-figure special assessments to current owners to fund decades of deferred maintenance. A $50,000-$200,000 special assessment on a $300,000 condo forces owners into selling, which drives prices down, which puts more owners underwater, which creates more forced sales. This is a mechanical process, not a confidence problem. Third: migration reversal. Domestic in-migration to Florida has collapsed 93% from its 2022 peak. During the pandemic, Florida was the primary destination for remote workers, retirees, and capital flight from higher-tax states. That flow has reversed. People who bought Florida homes in 2021-2022 at peak prices are now leaving (for cheaper states, for more stable insurance markets, for family) and putting those homes back on the market into a weaker demand environment.

- The structural comparison to 2008 matters. 2008 was a credit crisis. Subprime lending, no-doc mortgages, 2-28 ARMs resetting, securitization failures, Wall Street panic. The mechanism was universal across most US housing markets simultaneously. 2026 Florida is a specific structural stress. Insurance-driven cost pressure, condo-specific regulatory aftermath, migration reversal, climate risk repricing. The forces are Florida-specific, not national. The national housing market is actually performing reasonably well — foreclosure rates nationwide are 87% below the 2010 peak. Household equity remains at historic highs. Lending standards are stricter than the subprime era. A 2008-style nationwide crash is extremely unlikely. But Florida is different. Florida is what happens when climate risk, regulatory aftermath, and affordability pressure compound in a single state simultaneously. Three observations about what this means. First observation — the data suggests buyers have genuine leverage for the first time since 2020. Short sale inventory at 1,000+ listings, foreclosure rate doubling, 13 months of condo supply — these are buyer’s market conditions by every traditional metric. If you’ve been waiting for a Florida housing correction, you’re in it right now. Discounts of 20-40% below peak are available in specific submarkets. Second observation — the distress is geographically specific in ways that matter. Inland single-family in Jacksonville: fine. Orlando: fine. Palm Beach high-end: still appreciating. Older coastal condo in Cape Coral: disaster. Pre-Surfside building in Miami Beach with pending special assessments: terrible. Lakeland or Punta Gorda inventory: opportunity if you can stomach hurricane risk. Third observation — insurance is the forward-looking variable nobody’s pricing correctly. If Florida insurance premiums continue rising 15-25% annually (current trajectory), the affordability math gets worse every year. Currently $7,700/year on a $350K home in Cape Coral. Next year $9,000-$9,500. Year after that $11,000+. At some point the insurance cost approaches or exceeds the mortgage itself, which triggers more forced sales, which drives prices down further. This is a slow-motion structural repricing, not a sudden crash. The deeper point worth naming. Climate risk is being priced into housing markets in real time through insurance markets.

- Insurance actuaries don’t care about political debates over climate change — they care about actual loss experience, and Florida loss experience has been brutal. Hurricane Milton, Ian, and multiple other billion-dollar weather events have pushed reinsurance rates up, which flows through to primary insurance pricing, which flows through to monthly homeowner costs, which flows through to home prices. The repricing is working as intended. Markets are pricing climate risk where traditional political mechanisms have failed to. It’s just happening through a mechanism that crushes current homeowners rather than being distributed equitably across society. For investors: this is an opportunity with specific risk parameters. Cash buyers currently represent 33% of Florida transactions (67%+ in Miami-Dade luxury). They provide a demand floor. The distress isn’t leading to free-fall because institutional and cash buyers are stepping in on specific properties at specific prices. If you can analyze insurance exposure, condo association financials, hurricane risk, and flood zone classification — and you’re buying with cash or with non-Florida-contingent financing — there are genuine discounts available. If you’re using 80% LTV financing on a coastal condo with pending special assessments, you’re buying into a capital call scenario that could wipe out your equity within 18 months.

- The intelligence of buying in a distressed market is pattern matching the specific assets that will recover against the specific assets that will continue declining. Connect this to today’s broader content. The Trump “economy is booming” post this afternoon. The House Democrats affordability post. The car battery gouging post. The normalized scams post. Each one has been examining what affordability actually means in 2026. Florida housing is the biggest individual financial decision most American families will ever make, and it’s being restructured in real time by forces none of those political framings capture. Insurance pricing climate risk. Condo reserve mandates exposing decades of deferred maintenance. Migration patterns reversing as remote work culture normalizes. The affordability conversation in 2026 can’t be reduced to “Trump bad” or “Biden bad” or “inflation high.” It’s a series of specific structural repricings happening simultaneously across housing, insurance, healthcare, education, and consumer goods. Florida is the leading indicator for climate-adjusted housing markets. Texas Gulf Coast is next. California wildfire zones are already there. North Carolina coast is watching. A Florida house at a $100,000 discount isn’t just a deal. It’s a repricing signal. The buyers who understand the signal will position accordingly. The sellers who understand the signal already listed. The market does the repricing either way.

59 Banks Are Quietly Sitting on a $900 Billion Time Bomb (New Names Added Daily) Fifty-nine of the 158 largest banks in America are sitting on commercial real estate loans worth more than three times their entire capital cushion — and $875 billion of that debt is coming due in 2026. The list of at-risk banks is public. The names are alphabetical. Yours might be on it.

Elon Musk – 10 million views so far for the following book…

Lies My Liberal Teacher Told Me: Debunking the False Narratives Defining America’s School Curricula – Audio version available – I love Audio since I can keep working while listening and learning. – Sgt Pat

“As an Amazon Associate I earn from qualifying purchases.”

Movers & Shakers in Amazon Devices & Accessories

Our biggest gainers in sales rank over the past 24 hours. Updated frequently.

CLICK HERE FOR COMMENTS